The recent bank collapse of SVB and Signature Bank has many companies uneasy about the very institution of banking as well as the safety of their accounts.

We’d like to offer you several effective ways to ensure you’re safeguarding your funds.

- Think about your existing situation: Learn the mix of industries your banks work with. Ask for banking industry metrics and investigate how they compare. And look into programs that distribute funds in an insurable manner. The IntraFi program lets financial institutions offer depositors access to FDIC insurance for large-dollar deposits through a single financial relationship. You can keep all your money at the same bank and the network will channel your money into your choice of deposit accounts at other network banks. Another option is CDARs: Certificate of Deposit Account Registry Service® is a special system developed to provide large depositors better access to FDIC coverage for their funds. Find more information on IntraFi and CDARs at https://www.intrafinetworkdeposits.com/how-it-works/

- Review your distribution circumstances. Look into your current financial, capital and debt requirements and verify you’re not breaking any covenants. Excess cash can then be managed by individual owners, investors etc. Be sure your company has adequate cash reserves. Another idea may be to open a cash management account. The FDIC insures the cash balance of a cash management account, and some institutions offer coverage for up to $2 million as members of the IntraFi program.

-

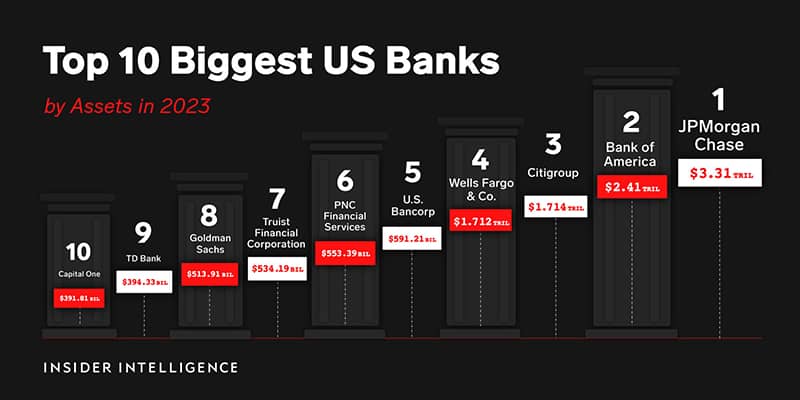

Consider opening an account with a larger, more established banking institution to spread out your funds. Here are the biggest banks based on assets.

source: https://www.insiderintelligence.com/insights/largest-banks-us-list/

- Think about adding joint owners to double the insured amount in your deposit accounts. Confirm with your bank that FDIC insurance would increase from $250K to $500K with joint owners. Or open an account that’s in a different ownership category; the FDIC covers many of these, including:

- Single accounts (one owner)

- Joint accounts (more than one owner)

- Certain retirement accounts

- Revocable and irrevocable trust accounts

- Corporation, partnership and unincorporated association accounts

- Employee benefit plan accounts

- Government accounts

- Use time to your advantage. For CD’s, be aware that you can manage these assets through other banks for 3-6 months in $250K tranches. CDARs (see #1 above) might be your better option for this purpose.

- Other ideas:

- Join a credit union. The National Credit Union Share Insurance Fund insures up to $250,000 per person, per institution, per ownership category at credit unions with National Credit Union Administration membership.

- Get an account that has FDIC and DIF insurance. The DIF is a private, industry-sponsored insurance fund that insures all deposits above FDIC limits at member banks. All DIF member banks are also members of the FDIC.

You can empower yourself and protect your business assets by researching your banking options. Feel confident your money is safe and look forward to a bright business future.

For more information on these options, or to review the specific needs of your business, contact VertexCFO.